Job Costing Versus Process Costing A Complete Guide

The whole debate boils down to a single question: Are you building one-of-a-kind projects or pumping out thousands of identical items? That’s the core of it. Think of job costing as the method for a custom cabinet maker, where every project is unique and needs its own specific cost tracking. On the flip side, process costing is for a factory that mass-produces stock plywood panels, averaging costs across the entire production run.

Understanding the Core Differences

Choosing between job costing and process costing isn't just an accounting exercise; it's a fundamental business decision that hits everything from profitability analysis to expense management. The method you pick has to mirror how you actually produce your goods. It will dictate how you quote jobs, value your inventory, and even prepare your financial statements.

To make the right call, you have to get into the weeds of what makes each approach tick.

- Job costing is all about the fine details. It’s for businesses where you can point to a specific job and say, "This project used these exact materials, this much labor, and this slice of overhead." You simply can't survive without it when every job is a world of its own.

- Process costing takes a bird's-eye view. Instead of tracking costs by the job, you accumulate them by department or production stage over a set period. It then averages those costs out, which works perfectly when you have a continuous flow of identical products.

This isn't just about picking a preference. Your choice reflects the very soul of your business model. When weighing your options, it's also a good time to think about the tools you'll use. Knowing how to choose accounting software that supports your costing method from the get-go can save you a world of headaches later on.

Job Costing vs Process Costing At a Glance

Sometimes a simple, side-by-side view makes all the difference. This table breaks down the fundamental distinctions between the two methods to give you a quick reference.

| Attribute | Job Costing | Process Costing |

|---|---|---|

| Primary Application | Unique, custom, or distinct products and services. | Homogeneous, identical products made in large volumes. |

| Cost Accumulation | Costs are collected individually for each specific job. | Costs are accumulated by department or process. |

| Core Document | Job cost sheet. | Departmental production report. |

| Unit Cost Focus | Determines the total cost of a single, specific project. | Calculates an average cost per unit for a large batch. |

| Typical Industries | Construction, custom woodworking, creative agencies. | Food processing, chemical manufacturing, oil refining. |

As you can see, the right choice becomes pretty clear once you define what you make and how you make it. One is built for specificity, the other for scale.

How Job Costing Drives Profit on Unique Projects

Think of job costing as a financial microscope for any business that builds custom products or provides specialized services. Instead of lumping all your expenses together and hoping for the best, this method meticulously tracks every single dollar spent on a specific project. It’s built for shops where no two orders are ever the same.

This approach essentially treats each job as its own little business, complete with its own profit and loss statement. Every component—from raw materials and labor hours down to a slice of the factory overhead—is tied to a unique job number. That kind of precision is absolutely critical in industries like construction, creative agencies, and custom manufacturing, where costs can swing wildly from one project to the next.

The Mechanics of Precise Tracking

The real workhorse of job costing is the job cost sheet. This is the master document, the central ledger for a single project. It collects all the expenses as they happen, giving managers a live look at the project's financial health.

This detailed tracking breaks down into three core components:

- Direct Materials: Every single board for a custom kitchen or every yard of fabric for a bespoke piece of furniture gets recorded against that specific job.

- Direct Labor: The hours a craftsman spends on a particular project are logged directly to it, ensuring you know exactly how much labor that job consumed.

- Manufacturing Overhead: This is for the indirect costs—things like the shop's rent, utilities, or a supervisor's salary. These are allocated to jobs using a predetermined rate, often based on something like machine hours or direct labor hours.

By linking costs so directly, you can spot budget overruns the moment they happen, not weeks later when it's too late. This kind of proactive control is a massive competitive advantage.

From Cost Data to Strategic Decisions

Job costing is far more than just bookkeeping; it’s a strategic tool. For decades, it's been the foundation for success in project-based work. A 2020 survey, for example, found that over 78% of construction firms rely on job costing systems to get a grip on their costs and track profitability, which naturally leads to more accurate bids and better win rates.

This detailed data gives you the power to see which types of projects are your real money-makers, which helps shape your entire business strategy. For any company doing project-based work, especially in construction, getting a handle on detailed construction job costing is non-negotiable for staying profitable.

By assigning every cost to a specific job, you transform accounting data from a historical record into a powerful tool for real-time decision-making and strategic planning.

Ultimately, job costing delivers the financial clarity you need to quote more competitively, manage your resources without waste, and make sure every single project pulls its weight. It all comes down to knowing your numbers, one job at a time—and that’s the key to real growth in any custom business.

A Look at Process Costing: Mastering the Unit Cost

While job costing gives you a microscope to examine one-of-a-kind projects, process costing is more like a wide-angle lens, perfect for mass production. This is the go-to method for companies that churn out huge volumes of identical or very similar products. Think about the bottling plants, chemical manufacturers, or phone assembly lines of the world—places where production is a continuous flow.

Instead of tracking costs for every single order, process costing groups them by department or production stage. All the raw materials, labor, and factory overhead for a certain period are collected for each step—like mixing, molding, or packaging. At the end of the period, you just take that big bucket of costs and divide it by the total number of units produced. The result is a simple, dependable average cost per unit.

Trying to do it any other way would be chaos. Can you imagine a soft drink company creating a separate job sheet for every single can of soda? It’s not just impractical; it’s completely pointless.

How Costs Move Through a Process System

The real dividing line in the job costing versus process costing debate is how expenses are gathered and assigned. In a process costing system, costs simply follow the product from one department to the next.

Let's walk through a basic two-step operation:

- Department A (Mixing): This is where it all starts. Raw materials get combined, and all the associated material, labor, and overhead costs for this step are bundled together. Once the batch is mixed, the product—and all the costs tied to it so far—moves on.

- Department B (Packaging): The mixed product arrives to be bottled and labeled. This department adds its own labor and overhead costs to the pile it just received from Department A. The final unit cost is the grand total of everything from both stages.

This sequential flow is what makes it work for industries built on continuous production. Process costing has been the standard for decades in sectors like food and beverage, chemicals, and electronics. In fact, research shows that 85% of large manufacturers in North America and Europe rely on it to manage their continuous production lines. When you're making over 1.7 million units an hour in one factory, there's just no other way. You can dig deeper into these manufacturing cost strategies on constructioncostaccounting.com.

The Strategic Upside of Averaging Costs

The real strength of process costing is its simplicity and consistency. In high-volume markets where profit margins can be razor-thin, this method gives you the solid data needed to set competitive prices and stick to them.

Process costing transforms a potentially chaotic stream of continuous expenses into a predictable and manageable financial metric, enabling stable inventory valuation and strategic pricing.

By averaging out the costs over thousands or millions of units, businesses can report consistent inventory values on their balance sheets. This also leads to a more reliable cost of goods sold figure on the income statement. That kind of financial stability is absolutely essential for accurate reporting and smart long-term planning, turning a complex, high-speed operation into something financially predictable.

Comparing Calculation and Reporting Frameworks

https://www.youtube.com/embed/nu4EPtIsZq8

Theory is one thing, but the rubber really meets the road when you look at how each costing system actually calculates costs and reports the results. The core documents and the entire flow of information are completely different, because they're built for entirely different kinds of work. One method is all about the individual project, while the other is designed to handle a steady, continuous stream of production.

At the heart of job costing is the job cost sheet. Think of this as the dedicated financial biography for a single project. It’s a running ledger that meticulously tracks every single expense—materials, labor, a share of overhead—tied directly to that job. This granular view is absolutely critical for custom work, giving you a real-time pulse on a project's financial health.

Process costing, on the other hand, operates on a much broader scale. Its key document is the departmental cost of production report. Instead of tracking individual items, this report pools all the costs incurred by a specific production stage (like mixing, baking, or packaging) over a set period. Its main job is to figure out an average cost per unit by dividing the department's total costs by all the units that passed through, including those still in progress.

Job Costing Example: A Marketing Campaign

Let's say a digital marketing agency is running a three-month campaign for a new client. The job cost sheet would be the single source of truth, capturing every specific expense to give a clear picture of the project's total cost and, ultimately, its profitability.

Here’s what a simplified version might look like:

- Direct Labor:

- Graphic Designer: 40 hours @ $75/hour = $3,000

- Content Strategist: 60 hours @ $90/hour = $5,400

- Direct Costs (Ad Spend):

- Google Ads Budget = $10,000

- Social Media Ads = $5,000

- Allocated Overhead:

- Based on 100 total labor hours @ an overhead rate of $20/hour = $2,000

Adding it all up, the agency gets a total job cost of $25,400. This isn't an estimate; it's a precise number. That figure is the foundation for accurate client billing and lets the agency analyze the campaign's true profit margin against what they charged.

Process Costing Example: A Bottling Plant

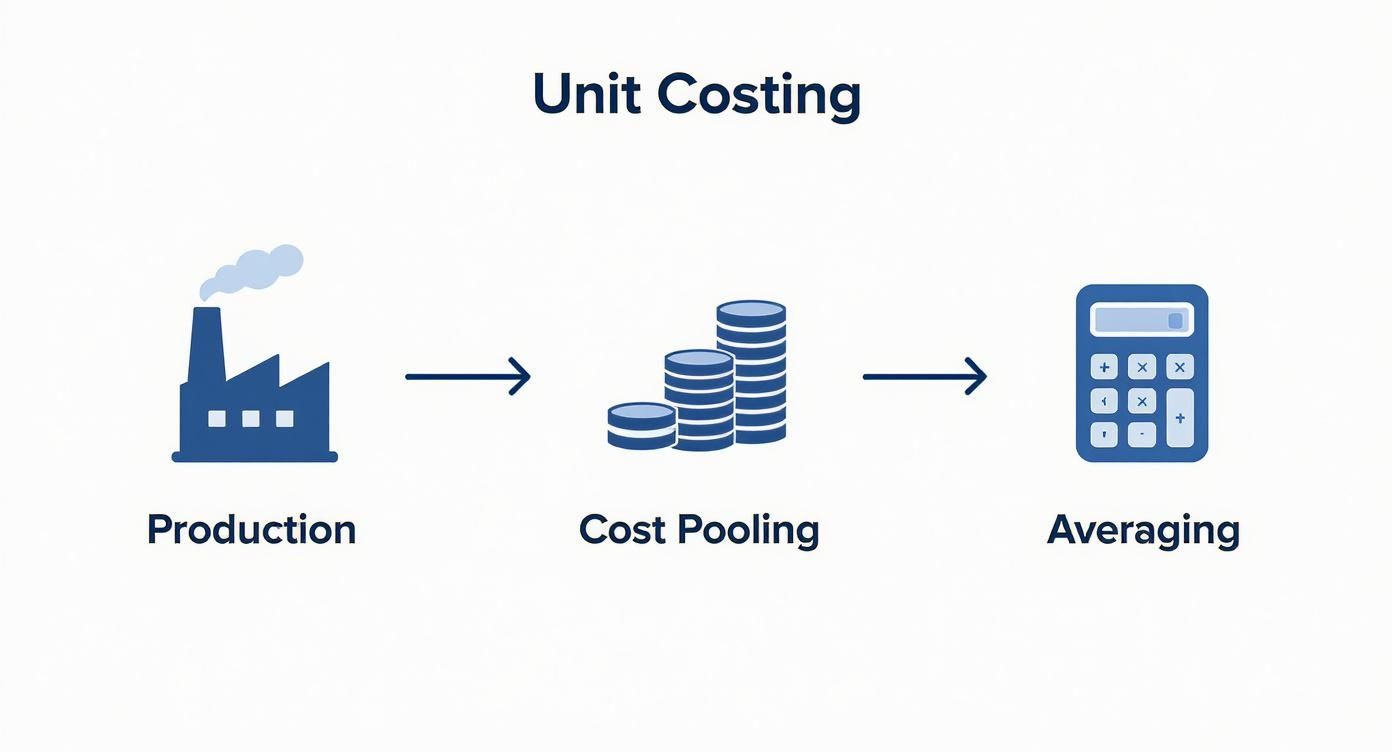

Now, switch gears to a bottling plant's packaging department. For a given month, the focus isn't on a single bottle but on the entire flow of production. The whole point is to find a reliable average cost for packaging one unit.

Process costing uses a clever concept called equivalent units to fairly account for all the partially finished items in the work-in-process inventory. This diagram shows how all production costs get pooled together before being averaged out to find the final unit cost.

As the visual makes clear, in a continuous system, the specific cost of one unit is irrelevant. What matters is the average cost pulled from the total pool of expenses.

Let’s say the packaging department racked up $200,000 in costs and produced 1,000,000 equivalent units during the month.

The math is simple: $200,000 / 1,000,000 units = $0.20 per unit.

This average cost becomes the bedrock for financial reporting. It’s used to value the finished goods moving to the warehouse and the inventory still left in the department. For high-volume industries, it provides the stable, predictable metric they need for pricing strategies and inventory valuation.

Impact on Financial Reporting and Decision-Making

The choice between job and process costing sends ripples through your entire financial reporting and decision-making structure. It's not just an accounting detail; it fundamentally shapes how you understand your own business. This table breaks down how each method directly influences pricing, inventory management, and profitability analysis.

| Business Function | Impact of Job Costing | Impact of Process Costing |

|---|---|---|

| Pricing Strategies | Enables cost-plus pricing on a per-job basis. Prices are set based on the actual costs incurred for that specific project, plus a desired profit margin. | Supports market-based pricing and long-term price stability. Prices are based on average production costs and competitive positioning, not individual unit costs. |

| Inventory Valuation | Work-in-Process (WIP) and Finished Goods inventory are valued at the actual cost of specific, identifiable jobs. Each item has a unique, traceable cost. | Inventory is valued at the average cost of all units produced during a period. Individual units are indistinguishable from a cost perspective. |

| Profitability Analysis | Profitability is analyzed at the individual job level. You can instantly see which projects, clients, or types of work are most and least profitable. | Profitability is analyzed at the department, process, or product line level. The focus is on the overall efficiency of production runs over time. |

Ultimately, each method delivers the right kind of data for its intended environment. A custom cabinet maker needs to know the exact profit on the kitchen they just built, while a soda bottler needs to know the average cost to fill a can. The data each system provides directly impacts everything from how you price your work to how you value your assets.

Making the Right Choice for Your Business Model

Choosing the right costing method is where your day-to-day operations really hit the books. The decision between job costing and process costing isn't just about what you make; it’s about how you make it, what your customers want, and how tightly you need to control your expenses to stay profitable.

It's rarely a simple, one-size-fits-all answer. Plenty of businesses walk the line between both production styles. Think about a local bakery: they might use process costing for their daily run of standard bread, where costs are simply averaged across hundreds of identical loaves. But for a custom, multi-tiered wedding cake? That’s pure job costing. Every single ingredient, every minute of a decorator's time, has to be tracked to make sure that one-of-a-kind project actually makes money.

Taking a Hard Look at How You Work

To pick the right method, you have to get honest about the fundamentals of your workflow. This isn’t just an accounting exercise—it's about understanding how your business actually creates value.

Start by asking yourself a few straightforward questions:

- Is my work project-based or continuous? If you’re starting and stopping for each unique customer order, job costing gives you the detail you need. If you're running a continuous line or large batches of the same thing, process costing is far more practical.

- Do my customers want custom-built or off-the-shelf? The more customization you offer, the more you need the pinpoint accuracy of job costing to price things correctly and protect your margins.

- How much control do I need over costs? Job costing is perfect for watching a budget in real-time for a specific project. Process costing is better for tracking the overall efficiency of a whole department over a period of time.

The Financial Impact of Getting It Right

Matching your costing method to your business model isn't a small thing—it can have a massive impact on your bottom line. A PwC study of 500 firms found that companies using the appropriate method boosted their profit margins by an average of 18%. More specifically, custom furniture makers who switched from a generic process approach to job costing saw their project profitability jump by 22%, which proves just how powerful precise tracking can be. You can learn more about how costing methods influence business outcomes on study.com.

The right costing system isn’t just for tracking expenses. It tells the financial story of your operations, which helps you make smarter calls on what to charge, what to build, and what services to offer.

For woodworking shops that juggle both standard stock items and custom builds, a hybrid approach is often the only way to go—and you need software that can keep up. Modern systems built for custom manufacturing can manage both worlds, making sure you capture every cost, whether it’s for a single unique piece or a big production run. You can see how today's platforms manage this complexity by checking out TimberCloud’s all-in-one features.

Integrating Costing Methods with Modern Software

Good cost accounting theory is one thing, but turning those principles into actual profit requires the right technology. Modern ERP and shop management software are the bridge, automating the tedious and complex data collection that both job costing and process costing depend on. This is how businesses finally move beyond clunky spreadsheets, cut down on human error, and gain a real-time view of their financial health.

Whether you’re building one-of-a-kind projects or mass-producing identical items, the right platform is non-negotiable. It delivers the accurate, immediate insights you need to stop guessing and start making strategic decisions.

Software Support for Job Costing

For any shop built around unique projects, the software has to be incredibly granular. The name of the game is capturing every single cost—materials, labor, machine time—and tying it back to a specific job number the second it happens.

Essential features to look for include:

- Real-Time Labor and Material Tracking: Think shop floor data collection—barcode scanners, tablets, or mobile apps that let your team log their time and the materials they use directly against a job. This eliminates guesswork and ensures every cost is assigned correctly.

- Automated Quoting Workflows: The best systems can generate a precise quote by pulling live material prices and your pre-set labor rates. Once the customer approves, that quote is instantly converted into a production order, saving hours of administrative work.

- Project-Specific Reporting: Good software gives you a dashboard with an at-a-glance view of a job's budget versus its actual costs. This is crucial for catching potential overruns early, while you can still do something about them.

Tools for Streamlining Process Costing

On the flip side, software designed for process costing is all about managing huge volumes of data and calculating averages across different production departments. The focus shifts from the individual job to the efficiency of each stage in the process.

The right software transforms costing from a historical accounting exercise into a dynamic, forward-looking management tool, providing the visibility needed to control costs and protect margins in real time.

Here, you'll need functionalities built for scale:

- Batch and Lot Traceability: Being able to track a batch of materials and its associated costs as it moves through each production stage is vital. This isn't just for accounting; it's critical for quality control and regulatory compliance, especially in industries like food processing or chemicals.

- Automated Cost Roll-Ups: Instead of manually adding up costs, the system does it for you. It automatically pools all expenses by department and calculates the average cost per unit, which makes generating production reports almost effortless.

At the end of the day, you need a platform that fits your workflow, not the other way around. Digging into the full range of shop management software features can help you see exactly how technology can automate these critical costing functions for your specific business.

Common Questions About Costing Systems

Even after you've wrapped your head around the theory, putting costing systems into practice brings up a lot of real-world questions. Let's tackle some of the most common ones that pop up when businesses try to figure this out.

Can a Business Use Both Methods?

Absolutely. In fact, many businesses do. Using a hybrid costing system is pretty standard for companies that have a mix of operations.

Think of a furniture company. They might use process costing for their standard line of kitchen chairs that they produce in large, identical batches. But when a client comes in asking for a one-of-a-kind, live-edge dining table, they'll switch to job costing to track that specific project's unique materials and labor. This hybrid approach gives them the most accurate cost picture for each part of their business.

What Is the Biggest Implementation Hurdle?

For job costing, the toughest part is almost always ensuring consistent and accurate data collection. It lives and dies by how well you track every piece of material and every minute of labor for each specific job. If your team isn't diligent about logging everything to the right project code, your data becomes useless, and the whole system falls apart.

For process costing, the main challenge is a bit more conceptual: getting your head around "equivalent units." This is the accounting trick used to assign value to inventory that's still in production.

The concept of 'equivalent units' is the mechanism process costing uses to accurately value work-in-process inventory. It translates partially completed items into the equivalent of fully completed ones for accounting purposes.

To dive deeper into manufacturing strategies and costing methods, check out more articles on the TimberCloud blog.

Topics

TimberCloud Team

Content Team

The TimberCloud team is dedicated to helping manufacturers streamline their operations with intelligent software solutions.